US Equity Fear Gauge Tops 2008 Crisis Levels as Short Interest Hits Multi-Year Highs

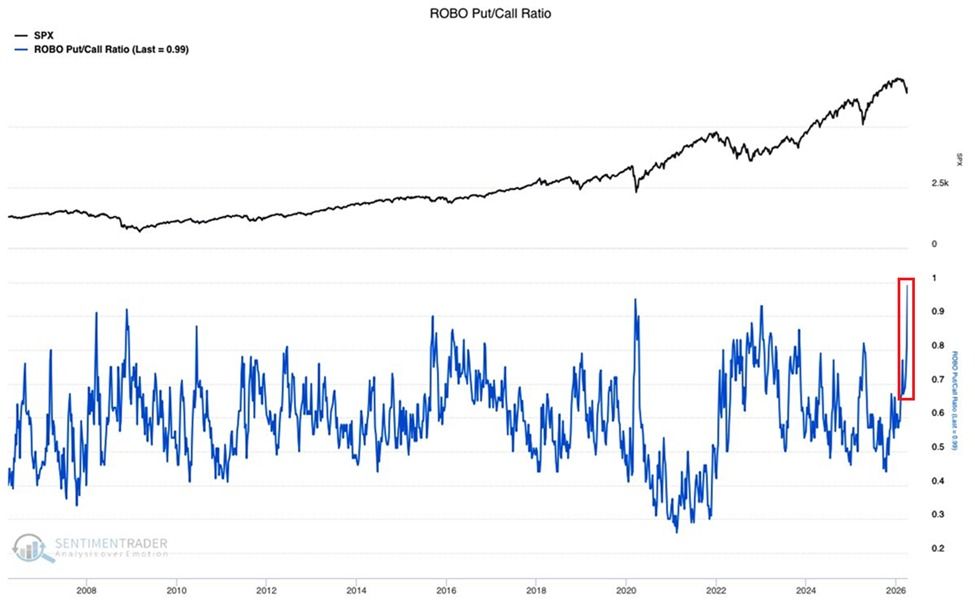

Retail fear across US equity markets has reached levels not seen in over two decades. The ROBO Put/Call Ratio has jumped to 1.0 for the first time in at least 20 years.

The reading exceeds the 0.91 peak during the 2008 Financial Crisis and the 0.95 reached during the 2020 pandemic selloff. The ratio has doubled since December, marking the sharpest rise since the 2022 bear market began.

“This ratio tracks retail opening buy orders in options, with the current reading showing retail traders buying nearly equal amounts of puts and calls…Fear is becoming overdone in this market,” The Kobeissi Letter noted.

Follow us on X to get the latest news as it happens

Market sentiment is also evidenced by the CNN Fear & Greed Index, which has fallen to 23, placing it at the threshold of extreme fear territory.

Bearish Positioning Reaches Rare Extremes

The surge comes amid a broad rise in short interest across all major US indexes. According to data from Global Markets Investor, the median short interest for the S&P 500 now stands at approximately 3.7%, its highest level in 11 years.

The Nasdaq 100 has reached roughly 2.7% short interest, a 6-year high. The Russell 2000 sits near 5.0%, its highest in 15 years.

The last time all three indexes showed such elevated short positioning simultaneously was during the 2010-2011 European debt crisis. That convergence is significant because it suggests bearish conviction extends beyond any single sector or market-cap segment.

“All three indexes have seen short interest rise sharply since mid-2024, accelerating further in 2026,” the post added.

BeInCrypto recently reported that hedge funds shorted global equities at the most aggressive pace in 13 years, with short sales outpacing long purchases by a ratio of 7.6 to 1.

The simultaneous alignment of extreme retail fear, a near-extreme Fear & Greed reading, and elevated institutional short positioning creates a notable asymmetry. Even a modest positive catalyst could trigger forced covering across multiple indexes, triggering a rapid, potentially disorderly rally.

The contrarian case is building, but a catalyst is needed. Sentiment alone doesn’t reverse markets. The critical question is whether current fear reflects genuine, fundamental deterioration or an overshoot driven by peak-fear psychology.

A resolution in the escalating US-Iran tensions could be the kind of macro shock that flips the narrative, but for now, with no signs of de-escalation, the market remains in a holding pattern between peak fear and potential inflection.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post US Equity Fear Gauge Tops 2008 Crisis Levels as Short Interest Hits Multi-Year Highs appeared first on BeInCrypto.

Read moreLatest News